.svg)

Understanding Recent Credit Market Headlines

Understanding Recent Credit Market Headlines

MLD

|

October 20, 2025

|

Chad Larson

Recent headlines about distress in segments of the credit markets have raised questions among investors. Most notably, First Brands Group, an auto-parts supplier, recently filed for bankruptcy protection. [1] Similarly, Tricolor Holdings, a sub-prime auto-financing dealer, has also filed for bankruptcy. [2] These events have sparked broader concerns in parts of the credit market, especially within the syndicated loan and securitized credit spaces.

It’s important to emphasize that:

- The companies currently in the headlines are not part of the private direct lending universe we are invested in.

- Your portfolio focuses exclusively on private direct lending strategies, which are structurally different and largely insulated from these developments.

What’s Actually Going On?

The current stress relates primarily to the Broadly Syndicated Loan (BSL) market and its securitized counterpart, Collateralized Loan Obligations (CLOs). These loans:

- Are underwritten and distributed by large banks

- Are often purchased by institutional investors via CLOs

- Are subject to mark-to-market volatility and sentiment-driven pricing

In the cases of First Brands and Tricolor, weaknesses in company fundamentals combined with over-leverage and opaque financing structures triggered distress. Due to their size and structure, these names were commonly held in syndicated and securitized portfolios. [3]

This has created ripple effects in the BSL and CLO markets, leading to wider spreads, technical selling, and broader investor caution. However, this environment has no direct bearing on the private credit direct lending strategies in your portfolio.

Why Private Credit Direct Lending Is Different — and More Resilient

Private credit direct lending refers to loans that are:

- Privately negotiated and typically held to maturity

- First-lien, senior-secured, and floating-rate

- Often provided in partnership with private equity sponsors

These loans are not traded, and they are not securitized. Instead, they are based on long-term relationships, bespoke structuring, and ongoing monitoring. They are not exposed to the mark-to-market volatility or forced selling that can occur in the syndicated markets.

This distinction matters. The performance of direct lending is driven by credit fundamentals, collateral value, and repayment ability — not secondary-market trading flows.

Your Portfolio: Five High Quality Direct Lending Strategies

Your portfolio is made up of diversified exposure to five high quality private credit direct lending strategies, managed by some of the most established investors in the space. Each is focused on senior secured lending to high-quality middle-market borrowers and operates independently of the BSL and CLO markets.

Of the five strategies, the four that target investments in the US are focused primarily on the more resilient upper middle-market/large corporate borrower segment of the market where company EBITDAs exceed $150 million. The portfolios are well diversified by industry sector and across many individual positions and primarily target sponsored transactions where the borrower is owned by a reputable private equity sponsor.

Sponsored transactions are typically regarded as being "less risky" given the sponsor’s significant equity investment in the company. On average, the LTV of the private credit funds held in the Alterna Portfolio is around 40%, meaning that on average, 60% of equity capital sits below the private credit lender in the capital structure. This level of equity subordination provides a meaningful "risk buffer" for the private credit investor.

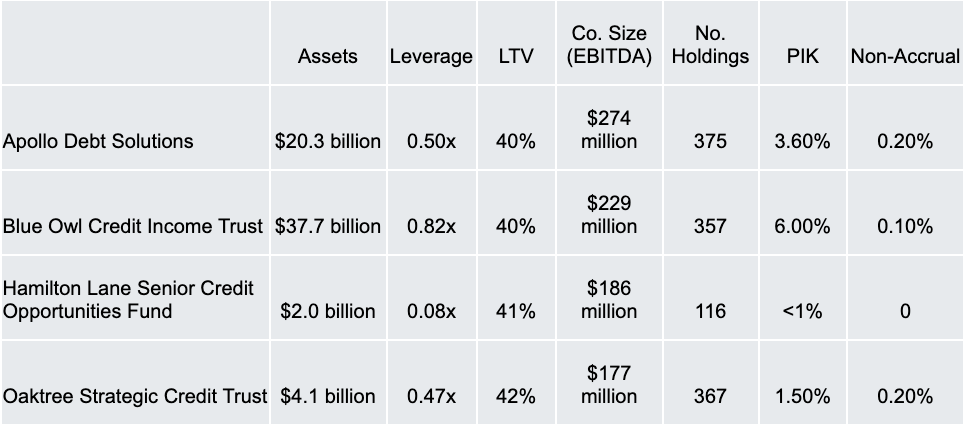

1. Blue Owl Capital – Blue Owl Credit Income Trust.

- Focus: Sponsor-backed, first-lien direct lending to large U.S. middle-market borrowers

- Portfolio: ~$18.6B in assets, 99% senior secured, 94% floating-rate

- Sector Exposure: Diversified across software, healthcare, business services

- Yield: ~10.3% net distribution yield (12-month trailing)

2. Hamilton Lane – Senior Credit Opportunities Fund (SCOPE)

- Focus: Diversified, senior secured credit to both sponsor- and non-sponsor-backed borrowers

- Portfolio: Over 200 issuers across more than 40 sponsors

- Structure: 100% floating-rate, 99% first-lien senior secured

- Return: 9.39% net (since inception), 8.75% distribution yield

3. Apollo – Debt Solutions BDC

- Focus: Senior direct lending to large-scale U.S. middle-market companies

- Portfolio: $3.5B+ net assets, ~96% floating-rate and first-lien

- Yield: 11.5% net distribution rate

4. Oaktree – Strategic Credit Fund

- Focus: Flexible private credit with majority exposure to senior secured direct lending

- Allocation: ~75% private credit, ~20% syndicated loans, 90%+ senior secured

- Portfolio: 93% floating-rate, 89% sponsor-backed

- Yield: Up to 10.38% annualized distribution

Bottom Line: Your Portfolio Is Insulated and Well-Positioned

Your direct lending investments are in a structurally different and more resilient part of the credit market. While headlines about syndicated loan defaults and CLO volatility may dominate the news, they have little to no connection to the strategies in your portfolio.

In fact, such dislocations often benefit direct lenders, who can step in and provide capital at attractive terms when banks and syndicated channels pull back.

You are invested in high-conviction strategies that prioritize principal protection, steady income, and disciplined underwriting—all outside of the noise currently impacting the securitized market.

Footnotes:

[1] https://www.reuters.com/business/finance/bank-america-among-lenders-bankrupt-first-brands-cfo-says-loans-are-secured-2025-10-15

[2] https://www.reuters.com/business/first-brands-tricolor-collapses-invite-more-scrutiny-wall-street-sees-robust-2025-10-14/

[3] https://www.ft.com/content/66f9bf5c-b412-4650-ab92-5b7d0d6ea002

[4] Blue Owl Credit Fact Sheet, August 2025

[5] Hamilton Lane SCOPE Fact Sheet, August 2025

[6] Apollo Debt Solutions Fact Sheet, August 2025

[7] Oaktree Strategic Credit Fact Sheet, August 2025