.svg)

MLD ALPHA-AI Portfolio Performance Update

MLD ALPHA-AI Portfolio Performance Update

AI

|

January 9, 2026

|

Chad Larson

MLD ALPHA-AI Year-End 2025 Summary

Investing where AI demand collides with scarcity

2025 further validated the core premise of the portfolio. AI is no longer just a software story. It is an infrastructure buildout shaped by real constraints: power availability, grid interconnection, base load reliability, and the metals required to electrify and cool the system. Several year-defining developments shifted the narrative from future demand to signed contracts, committed capital, and government-backed industrial policy.

Portfolio-Level Performance

Launch Date: November 24, 2025

Valuation Date: Current prices provided

Holding Period: ~42 days

Period Return: +7.89%

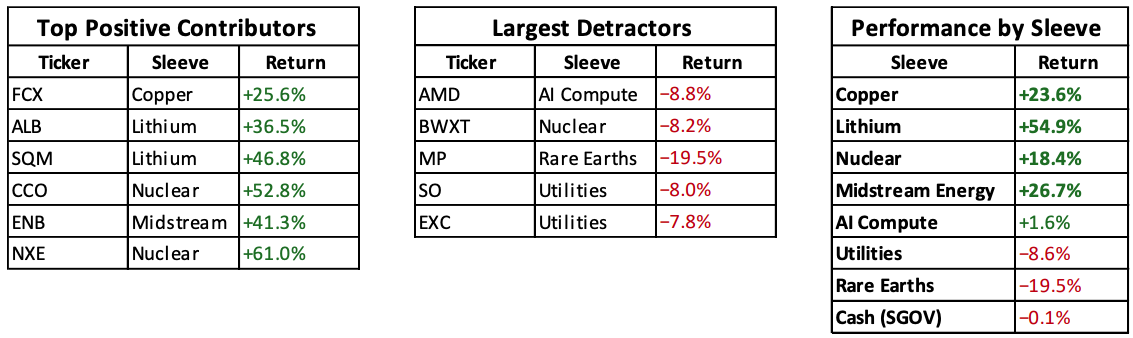

Key takeaway: Returns are being driven exactly where the thesis predicted: materials, nuclear fuel, and energy infrastructure, while compute has consolidated and regulated utilities lagged.

Structural Interpretation

The portfolio is working as designed:

- Early-cycle commodity and power scarcity assets are leading.

- AI compute is stabilizing after an extended run.

- Regulated utilities are lagging but providing ballast.

- Energy-transition convexity (lithium, uranium, copper) is dominating early returns.

- Volatility is productive, not destructive. Gains are broad-based across multiple sleeves.

Investable Themes That Strengthened in 2025

1. AI Load Became a Grid Constraint Story

By year-end, AI data centers were increasingly treated as a structural load shock to the grid, with power availability and cooling emerging as gating factors.

Why it matters: Utilities with constructive regulatory frameworks, plus gas and nuclear baseload suppliers, become picks-and-shovels for AI adoption.

2. Corporate Nuclear PPAs Became Bankable

Constellation’s 20-year nuclear PPA with Meta covering 1,121 MW marked a major inflection point.

Why it matters: Nuclear transitioned toward contracted infrastructure, supporting rerating potential for operators and uranium suppliers.

3. Energy + Big Tech Partnerships Scaled

NextEra’s expanded partnership with Google Cloud and multi-gigawatt commitments reinforced new AI procurement models combining power, campuses, and grid optimization.

Why it matters: A clear blueprint emerged for regulated utility winners.

4. Copper Scarcity Became Investable

Supply deficits deepened as electrification demand accelerated and disruptions mounted.

Why it matters: Copper remains a strategic bottleneck for AI and electrification.

5. Rare Earths Received Policy Backing

MP Materials secured Department of Defense support, including price floors and long-term offtake.

Why it matters: Strategic materials moved from speculative to policy-backed cash flow visibility.

Portfolio Company Highlights

AI Compute & Semiconductors

Compute remains central, but incremental returns are increasingly driven by infrastructure bottlenecks, not raw chip demand.

Investable takeaway: The constraint has shifted from silicon to power, grids, and materials.

Nuclear & Uranium

Existing nuclear fleets are being financially re-underwritten through long-term corporate contracts.

Investable takeaway: Nuclear has shifted from narrative-driven to bankable infrastructure.

Regulated Utilities & Grid

AI-driven load growth is expanding rate bases, though timing remains governed by permitting and interconnection.

Midstream Infrastructure

Gas infrastructure is increasingly critical as reliability backstops AI-era power demand.

Copper

Supply deficits and long lead times continue to skew risk to the upside.

Lithium

A cyclical market within a secular buildout, with advantage to low-cost, disciplined producers.

Rare Earths

State-supported industrial capacity has materially changed the risk profile.

What We’re Watching Into 2026 (High-Signal Catalysts)

- Additional hyperscaler PPAs for firm power and implied scarcity pricing. - Canary Media

- Transmission buildout and interconnection acceleration. - Utility Dive

- Copper deficit confirmation and supply disruptions. - Reuters

- Execution milestones across rare earths, uranium, and midstream assets. - Reuters